Using an RRSP to Reduce Your Taxes and Buy a Home!

Are are looking to get into the housing market and purchase your first property in the next little while, but saving a downpayment is proving to be difficult? Here is a simple strategy that could help you out!

Let me show you how purchasing an RRSP with the money you have already saved up can actually give you a larger downpayment down the road.

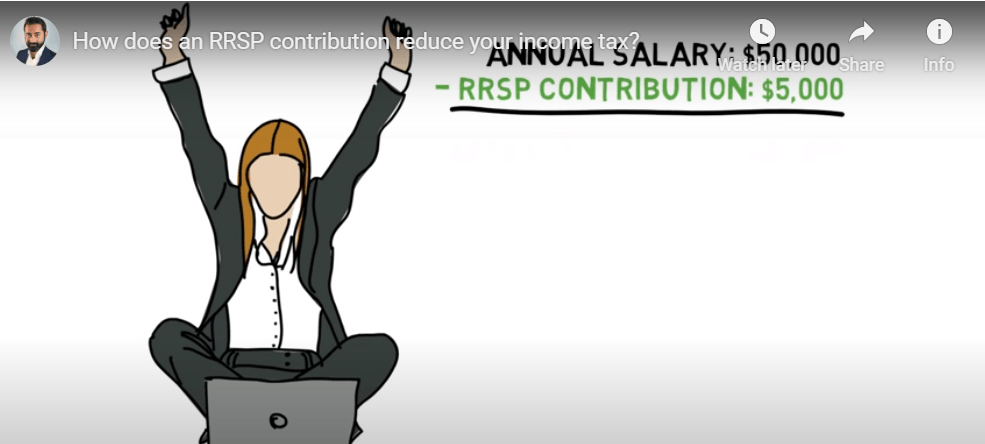

First off, in order to understand the strategy, you have to understand how an RRSP works. Here is a very easy to follow video by Preet Banerjee (Canadian Finance Personality) that explains how an RRSP contribution reduces your income tax. If you haven’t already, take the 3 minutes and watch the video!

So in the video, we learned how Susie Salary took an income of $50k a year, purchased a $5k RRSP in order to trigger a tax refund of $1750. If Susie is buying her first home, she now has $6750 to use for a downpayment, this is because in Canada money in an RRSP can be accessed for a downpayment through what is called the Home Buyers Plan.

So to execute the strategy, you simply take the downpayment you have saved up, purchase an RRSP in order to trigger a tax refund. You then purchase another RRSP when you get your tax refund from the government. From there you will have access to all the funds through the Home Buyers Plan. And as an added bonus, the RRSPs purchased with your refund will actually lower your 2015 taxes as well!

From the Canada Revenue Agency Website:

The Home Buyers’ Plan (HBP) is a program that allows you to withdraw funds from your registered retirement savings plans (RRSPs) to buy or build a qualifying home for yourself or for a related person with a disability. You can withdraw up to $25,000 in a calendar year.

Generally, you have to repay all withdrawals to your RRSPs within a period of no more than 15 years. You will have to repay an amount to your RRSPs each year until your HBP balance is zero. If you do not repay the amount due for a year, it will have to be included in your income for that year.

Here are some of the highlights of the Home Buyer’s Plan

- Funds have to be in the RRSP for a minimum of 90 days before withdrawal.

- Maximum amount of funds to be used is $25k per person, $50k per couple.

- All funds have to be repaid over the next 15 years.

- You must be considered a first time home buyer.

The RRSP contribution deadline for the 2014 tax season is March 2nd 2015.

What do I do now?

Now, if you are relatively new to financial products and you aren’t all that comfortable just walking into your financial institution to purchase an RRSP, that is okay.

You might be thinking, “What if I purchase the wrong kind of RRSP, maybe I won’t be able to access it through the Home Buyers Plan? The deadline is coming up quickly and I don’t want to make a mistake.” Don’t panic. You can actually “park your RRSP in cash”. Which means you simply invest your cash into an RRSP, it will then trigger the refund and you will have full access to your funds when the time comes to use them as a downpayment.

Obviously you will want to discuss your financial situation with an accountant or tax specialist to see exactly how much of a refund you can expect to receive (and then reinvest) in order to purchase a home. If you don’t have a tax specialist, I would love to recommend someone. Likewise, you will want to consult your mortgage professional for professional mortgage advice… that is where I come in. I would love to work with you!

So, if you are planning to purchase a home in the next while, we should probably sit down and work through your numbers. I would love to help put together a plan and when you are ready to buy, I will help you arrange mortgage financing.

It’s never too early to involve me in the home buying process. Planning ahead is the best plan!

Feel free to contact me anytime, I would love to talk with you!

Katherine Martin

Origin Mortgages

Phone: 1-604-454-0843

Email: kmartin@planmymortgage.ca

Fax: 1-604-454-0842

RECENT POSTS